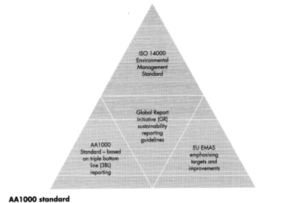

Social Accounting:

It is a concept describing the communication of social and environmental effects of a company’s economic action to stakeholders.

Triple Bottom Line accounting is one of the better way for social accounting.

Environmental Accounting:

Environmental accounting relates to the need to establish and maintain systems for assessing the organisation’s impact on the environment.

EMAS and ISO 14000 are both systems that support the establishment and maintenance of environmental accounting systems.

There are various reporting guidelines have been developed for Social and Environmental Accounting.

1) Triple Bottom Line Accounting:

TBL accounting means expanding the traditional company reporting framework to take into account environmental and social performance in addition to financial (economic) performance.

The concept is also explained using the triple ‘P’ headings of ‘People, Planet and Profit’.

People | The equivalent of social accounting (for example, the amount of charitable donations made) |

Planet | A focus on environment performance such as waste management and recycling targets |

Profit | A measure of the success of the business, but considering the redistribution of wealth which brings benefits to the local community (for example, education schemes and community projects) |

2) Global Reporting Initiative:

The Global Reporting Initiative (known as GRI) is an international independent standards organization that helps businesses, governments and other organizations understand and communicate their impacts on issues such as climate change, human rights and corruption.

Under increasing pressure from different stakeholder groups – such as governments, consumers and investors – to be more transparent about their environmental, economic and social impacts, many companies publish a sustainability report, also known as a corporate social responsibility (CSR) or environmental, social and governance (ESG) report. GRI’s framework for sustainability reporting helps companies identify, gather and report this information in a clear and comparable manner.

3) Eco – Management & Audit Schemes (EMAS):

EMAS is the Eco-Management and Audit Scheme. It is a voluntary initiative designed to improve companies’ environmental performance.

EMAS requires participating organisations to regularly produce a public environmental statement that reports on their environmental performance.

Accuracy and reliability is independently checked by an environmental verifier to give credibility and recognition to that information.

EMAS requires participating organisations to implement an environmental management system (EMS).

There are four key elements of the scheme:

– Legal requirement

– Dialogue/reporting

– Improved environmental performance

– Employee involvement.

4) ISO14000 (Environmental Management Standards):

ISO14000 is a series of standards dealing with environmental management and a supporting audit programme.

The ISO formulates the specifications for an EMS.

EMAS compliance is based on ISO 14000 recognition – although many organisations comply with both standards.

ISO 14000 focuses on internal systems although it also provides assurance to stakeholders of good environmental management.

To gain accreditation an organisation must meet a number of requirements regarding its environmental management.